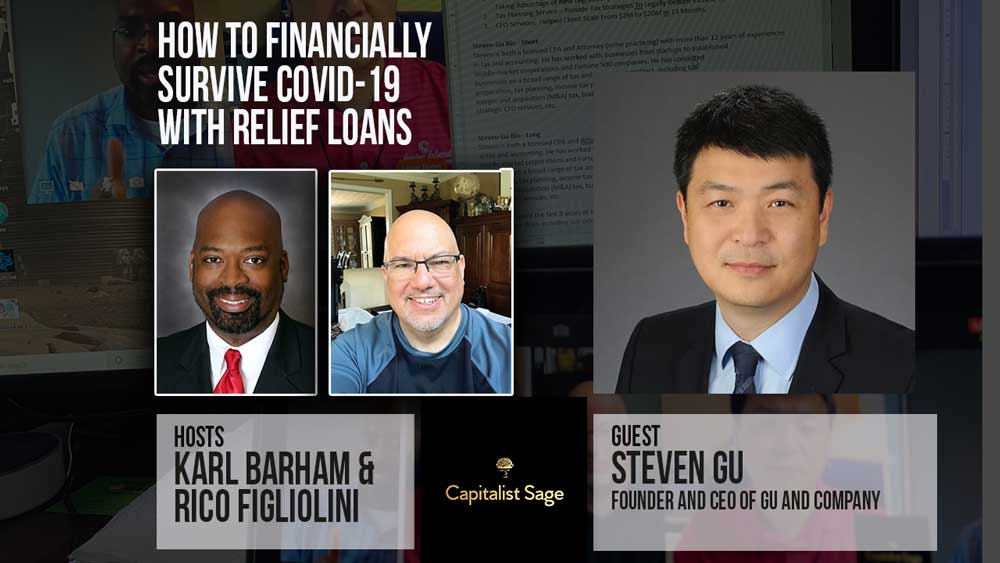

Business taxes and financials are already tricky enough to navigate, but with loans and other financially related acts surfacing in a response to COVID-19, the financial waters are even harder to tread. Luckily, in this episode of the Capitalist Sage, Steven Gu founder and CEO of Gu and Company shares some of his professional insight. Join Karl Barham, Rico Figliolini, and GU as they discuss PPP loans, the Care Act, COVID-19 response, and much more.

“We went through a change a little bit. When we do the tax plan before pre-COVID-19, we always try to focus on how to save people money. But now we are looking, not just at saving people money, saving people tax, but also helping them to generate cash. Bringing the cash to your pocket right now.”

Steven gu

Timestamp:

[00:00:30] – Intro [00:02:49] – About Steven [00:04:23] – Preparing for the Crisis [00:07:06] – The Loan Process [00:09:13] – Large Banks vs. Community Banks [00:13:57] – Changing Laws [00:24:09] – The Tax Benefit Buffet [00:30:16] – Long Term Planning [00:35:02] – Closing

Podcast Transcript

Karl: [00:00:30] Welcome to the Capitalist Sage podcast. We’re here to bring you advice and tips from seasoned pros and experts to help you improve your business. I’m Carl Barham with Transworld business advisors, and my cohost is Rico Figliolini with Mighty Rockets, digital marketing, and the publisher of the Peachtree Corners Magazine. Hey Rico. How you doing today?

Rico: [00:00:47] Good Karl. Thank you.

Karl: [00:00:49] Why don’t we get started by introducing our sponsors?

Rico: [00:00:52] Sure. Our lead sponsor for this show, as well as the other family of podcasts that we do is Hargray Fiber, and just want to introduce them. They are a regional company that handles cable fiber, optic connections. Bandwidths large for small businesses, as well as enterprise sized businesses. Providing solutions for collaborative work, providing bandwidth that’s needed for teleworking and being able to provide solutions for businesses of all sizes, customized to what they need. And they’re not the cable company, I can say that they’re not Comcast, they’re not AT&T. They are actually in your community providing services to the community and they’re there to be able to come to your door when you need them. So check them out. That’s HargrayFiber.com, or you could go to Hargray.com/business. Thank you.

Karl: [00:01:45] Oh, that’s fabulous. It’s great to see businesses that are focused on the business community here in Peachtree Corners and surrounding areas. Today, I am so blessed to get to introduce everyone to Steven Gu, who is the founder and CEO of Gu and Company, a fractional CFO tax and business advisory firm that services small and medium sized businesses. Today, we’re here to talk about EIDL loans, PPP loans, the Care Act, COVID-19 response. Lots of people have been going through reopening now. They’ve secured loans from the government and from their banks and they need to know what’s next. So we figured we’d have a conversation about that today. Hey Steven, how are you doing today?

Steven: [00:02:35] I’m good. How are you Karl? Hey Rico.

Rico: [00:02:38] Hey Steven. I gotta say thank you by the way, because I personally use Steven to help me get my PPP loans. So thank you for helping me do that.

Steven: [00:02:47] No problem.

Karl: [00:02:49] Cool. Well, you know, Steven here on the Capitalist Sage, we’re here to try to help people understand different things they can do to help their business. And we’ve been working over the last several months in helping business owners with cashflow leads. And how to access these PPP loans. But before we talk a little bit more about that, why don’t, why don’t you introduce yourself and tell us a little bit about why you do and how you got to do what you do today for so many business owners.

Steven: [00:03:19] Sure. Like you introduced me, you know, we normally what we do is really tax planning and that fractional CFO service, but during the COVID-19, we helped a lot of you know small, medium businesses really helping them to secure that EIDL or the PPP loan. And also there’s other financial resources available. So that’s our mission to help them to locate as a financial security, financial, to have them survive that COVID-19. And right now, we are at the second stage. So there are lots of business already called their PTP loans. So in a way, we are helping them how to plan the PPP loan, how to know how to use them, how to use a fund. So that as those money could be forgiven and also there’s other resources, other tax incentives, tax aids, and also you know, forecasting, budgeting, how to basically help them to survive and thrive during this COVID-19.

Karl: [00:04:23] You know, so many business owners when this started were caught and were surprised by the impact on people from a health standpoint. I remember, you were one of the first people starting to warn and advise of the impact of it. Tell me a little bit about how you were able to start seeing this coming. And some of the things you started learning that we needed to do when the crisis started.

Steven: [00:04:58] Right. Actually Karl, you’re one of the people sort of bombarded by me, you know, talking about a PPP for almost three months now. And you probably didn’t know, I think way back in, in March, around the middle of March. You know, you heard me talk about the idea or the talking, sometimes they don’t, they have no word for the PPP yet right? And then we started helping people get the idea, because know, when we have our cloud, we realize this COVID-19, this how bad it’s going to impact business. And we’d realize they are EID available. So we start to reach out to our clients, tell them one, you have to look at how much cash reserve that you have. And the two is like how to take advantage of all those financial aid available. That time is just a family, family first act. Like, so we started that and that time we went a platform, the idea was a website just crashed. At the time is the only, think it’s only a $6 billion. We would apply the website crashed all the time. We don’t really know where you get, it took us, like literally 12 hours to apply for one client. And it often would get done and then the website crashed multiple times. And then in April, early April, the CARES act came out and they added the 10K advanced payment, you can repress the 10K that’s where the 10k come from. It’s added by the CARES act. And then, because, I think as they probably lost it in beta, so they said, Hey, you know, whatever you submit on account, you have to reapply. And that then made is that the bit of the process extremely simple. Now you go there, you just need to spend less than five minutes. Just go submit your request of 10K. So I could, so before that, it’s very, very complicated. So that’s how it started. And at that time though, people, when we talk about a PVP, you know, if you’ve talked to other folks in your, nobody, nobody’s talking about that. But nowadays, if you go there and talk to other CPA, other advisors, probably they talk nothing but for PPP, but it’s a journey.

Karl: [00:07:06] There was a dynamic that happened in this, about getting to the front of the line. Those that had people that one, knew how to, knew the urgency of getting these funds and the necessity for cash in their business, along with how to do it, what documents and information was going to be required. I noticed how those people with that finance support were able to get to the front of the line and get loans. When, when folks got through that, what were some of the things that, that you saw small business owners didn’t do properly that might have delayed their ability to get some of these funds? What were some of the challenges you saw in some of your early clients in getting funding?

Steven: [00:07:56] Well, first of all, you know, for funding, they typically wait. Let’s say, a typical people is going to screw these up is you know, they don’t have a sort of financial statement, right? For the business, right? And you know, some, some businesses, they don’t even issue a W2 and that they not pay for payroll tax, right? Those are screwed the most. Basically, those are document that the bank files when you file a QPP. And the other issue we also see is really, you know, the financial, it’s not a, not ready. And, you know, tax returns are screwed up and also they’re sort of, they can do to themselves, this thought of the bigger bank is going to help them. And they, they’re just keying in a number they saw just in the application form. And they eventually going to turn it down. We saw that multiple times people just put whatever number they think. And then eventually the back comes back to, Hey, this is not accurate. And you have to wait for another one. And then first of all, the money by now, you come to the last month and the other millions of people ahead of you. So we definitely see people screw up because of that.

Rico: [00:09:13] Let me ask you something, Steven, when you helped me out, actually it was. We will be, they were between legislation, right? The second time it was coming up. We had,actually had talked about putting together the package and, we were ahead of before the legislation passed. So we were doing it ahead of time, right? Hoping that knowing sort of 90% sure that legislation was going to pass. So we were ahead of the curve a little bit, but I had other the friends that were out there that were applying through banks. And what I realized is that you can’t, you know, at the time anyway, many banks did not want to deal with you unless you had an account with them. Or you might’ve had an account with them, but you weren’t big enough.

Steven: [00:10:02] Yeah.

Rico: [00:10:03] In essence, Chase bank, wouldn’t be able to do what you want that maybe a smaller bank could or regional bank. So that’s, that’s where I saw the advantages, right? Does that make sense? Is that what you saw during that time?

Steven: [00:10:17] That’s exactly. Because, you know, we were monitoring this CARES act way before they passed, right? You know we, we read the Congress version of the PPP act. We read the earlier version, right? So we sort of know what’s going on before Trump signed that into the law. And then before he signed it into the law, we have to, we’ll started communicate the ways that different bank offers SBA lending, right? And to our surprise, we thought the bank, were excited. It’s sort of, they’re going to make lots of money. We realize the bank is not a, it’s not a very interested, especially, bigger bank. That’s to know that they cannot make too much money out of this and they’re employees are like, I have to wear the masks, go to the bank and apply, document all these things. They are not incentivized at all. And then we realized, Oh, this is going to cause a big problem, right? Because, and also they told us like, look, we’re going to take care of our prefered customers first. I mean, it makes sense. I mean, if I’m the business owner, I would take care of my you know, the important clients first. So that’s when we realized this way, would be like, you know, is this a web of chaos? Right? And the bigger bank does not necessarily give you the best service. And they don’t necessarily have your best interests in their mind. So that’s why, that’s when we tried to persuade people, try to tell people, let’s say look, if possible, you know always go to the community bank. A small bank that you have strongest relationship that they can take care of you. They can look at to return and look, look at your application, not necessarily the bigger banks. But at that time, lots of people do not trust us. And they’re like, Oh no, I’ve been dealing with Wells Fargo for how many years. I think first of all, we’re smarter than that, you know they try to game the system. They tried to get away from doing this. This is the first time the community bank really represented the meaning of community.

Karl: [00:12:21] You’ve highlighted a key lesson that a lot of successful business owners have learned is when the crisis hit, everyone ran to their safe place. But those that had built a relationship with their local community banker. And local community banks, they saw an advantage in this particular case to do that. And we always try to advise business owners to make sure they’re having relations. We’re not saying you shouldn’t do banking at the big banks. But you should also have a relationship with the community banks who’s able to pivot, move quicker. They know who you are. They get to understand what you need and be able to provide that service to you. But I think you highlighted something else that I wanted to make sure folks realize. The people that were able to get the loans and the funding first had payroll records. They had their financial statements ready. And I know a lot of people may wait til tax time to reconcile their financial statements if they have it. But if you ever need to go to a bank or a lender, all of those records are going to need to be done. And that just really shows as a business owner. There’s an element of the business of keeping up the financial records and your scorecard that’s important to be able to react quickly should the business environment pivot.

Steven: [00:13:55] Right.

Karl: [00:13:57] So now that we’ve gotten the loans and folks have gotten the funding. I’ve seen some news come out about more laws and more rules. And when it comes to, can you explain the difference between what originally people signed, everything got easy and they just signed something. But when they signed the first time, what were the terms of those loans that they got. Why didn’t they have to pay it back? What did they have to spend it on? And has there been any changes in that in recent weeks?

Steven: [00:14:29] Yes, great question. So this is the first time I, you know, I ever deal with that. So, so much uncertainties. You know, for the PPP application itself, the department of treasury and the SBA, they issued more than 20, like rulings and guidelines more than 20 times, right? And now after people get the money, they issued a new ruling that May 16. So they issued as that people that got PPP forgiveness, the preparation for. And a few days later the department of treasury issued a regular issue to some guidance on how to calculate the forgiveness portion. It’s, the application, PPP forgiveness application form it’s 11 pages. And as a department of treasury guide is 26 pages. Okay. And then, two weeks later now we just had a PPP flexibility act. It changes lots of things. Lots of important things, a lot of forgiveness. So it’s, it keeps changing, keep changing. So, yeah, there’s a few, let’s talk about before change. Before they make the big, before the flexibility act, they passed the law, the requirements are, you know, the money you receive. 75% of the money received has to be used on payroll and then for the remaining you can only use multi-interest, rent, or utility. Only those three, okay? And also you are required to remain a payroll number, right? A head account let’s say a full time, full time equivalent, meaning full time. Or if you have part time, you have to convert the part time into full time. Okay, so FTE, full time. So you have to maintain those payroll numbers, okay? People, how many people you have, and then you also are required to maintain the payroll level. If your payroll is reduced to more than 25% compared to prior quarter, the forgiveness amount will be reduced accordingly. A secondary requirement. That’s third requirement, the fourth requirement is you have to restore your employee headcount by June 30th. And if you don’t, then the forgiveness portion will be reduced. That’s another law. Right now under the, under the flexibility act. The 75-25 split has been changed to 60-40 split, I’ll explain why, okay? That’s one big portion. And also, previously you have, you have eight weeks to use this PPP money, eight weeks. And then, now they extended to 24 weeks. So you have more, you have more time to, to use up this PVP money, okay? And previously you only have up until June 30th to rehire, to restore your employees. But now you have up until the end of the year, okay? And, and also previously, if your PPP law is not forgiven, you have to pay back. You have two years to pay back. And then now they extend to five years. Okay, you have five years to pay it back. Okay.

Karl: [00:18:20] Why do you think, why do you think they did, they made these changes? What was the concern? What were they trying to address that they saw happening?

Steven: [00:18:29] The biggest one, there was a few things. If you think about it, once people get the money, think of a restaurant, okay? Once they get PPP money, they cannot basically, they cannot use the money for the, well that can, but even if you got the money, you probably see lots of employees they refused to return back to work. Why is the conditionings not permitted, it’s still unsafe or the restaurant simply is not open yet, right? And the third problem is really the restaurant owners are now competing with unemployment benefits. In California, for example, California state pays the employee people for like $550 a week. And the federal government matched another $600. So that’s like the people, people got to like $4,400 a month tax free, just unplanned benefit. So they are not like, they don’t want to, I make it for your, for your PPP, how much you pay for them, for the people working is probably less than $4,400. So they’re like, I would rather just stay at home, watching Netflix. I don’t want to go back to work, right? That’s why. And then for other businesses, they are really not ready to go back to business yet, right? So that means really, yeah you help the employees, but they are not ready to help as an employer because the money you’ve got already doesn’t help you restore, reopen the business, right? And so that’s why they extended that, extended the time. So say, okay, you don’t have to use it within eight weeks. You can use it within 24 weeks so you can decide, okay, I want to restore, I will ask the five people back first and then I’ll add more and more and more. Now it really makes sense now, right? And also I get previously, like if I want to use a PPP minus, so if my employee doesn’t want to come back, should I call the state to report them? If I report to that guy he’s not getting any benefit anymore. So it was putting the employer in a very odd situation, but now you don’t have to do that because now you have up until the end of the year to rehire all the people, right? So that’s, that’s the main, that’s the main concern. The other, there was also other people, like, again, they extended to rehire period back to, pushed it back to December. So the first period that’s kind of the same concern, like, Hey, If people, what if people don’t want to come back? Or what if you know, the condition is not ready to reopen yet. So really we give people more flexibility. And plus previously you only have eight weeks to pay, to use our money basically caused some issue because you got a 2.5 of your month to payroll that’s your PPP loan. And you’ve only got two months to use it. So you really have to think about what’s the way to use it right? I have to use it on something now. But now they give you more time. So really the policy is really want to make sure you know, almost everybody can get the money, be forgiven.

Rico: [00:21:45] It sounded like, it sounds like to me, the original policy was meant to be a shot into the economy to get it moving at a point where it’s stuck in the mud and it’s not going to move, right? I mean, people, customers are not coming back as quickly, right?

Steven: [00:22:02] Right.

Rico: [00:22:03] So you got that, and you’re right about unemployment. Now unemployment runs out that extended unemployment, I think in July.

Steven: [00:22:10] July 31st. Yeah.

Rico: [00:22:11] Right. So once that runs out, one of the restaurant owners I’ve spoken to, he’s like, you know, the problem is he says, is that they don’t want to work. Like you said, because maybe they’re getting more money.

Steven: [00:22:24] Yeah, exactly.

Rico: [00:22:25] By the time they come back. Some of these restaurants may not, some of them may not reopen anymore.

Steven: [00:22:30] Right.

Rico: [00:22:31] But we hope the majority will, and there won’t be as many jobs. So they’re looking at short term money. As, as versus looking at the long term, if they’re going to have the job three months from now or a month from now.

Steven: [00:22:44] Exactly. So that comes right down the mix, especially for tip workers. Like, you know, if I hired them back, for two months and then do I just fire them again, because we’re not ready? It’ll make no sense.

Rico: [00:22:55] Yeah. And then some companies who did we talk to that was, they had the cheese business, I think. And, essentially, Oh, you weren’t in that this was a different zoom podcast, but it was a cheese manufacturer, small business you had about 50 employees. She couldn’t let go of her employees. She had to use the money. Cause how can you retrain cheese manufacturers? If you will. It’s not a job…

Steven: [00:23:22] Right.

Karl: [00:23:24] They, folks once you let people go, they might find other jobs and other places and they won’t be able to bring them back. So those are some of the things that people have to pay attention to for the PPP. They’ve gotten some flexibility, some bandwidth. What about on the tax front? I know we would, they’ve got a delay to, a six month delay or one quarter delay, excuse me, for tax from April 15th. What’s the new current deadline for tax filing it? What does it mean for business owners? What do they have to pay attention to in filing their tax? Do they have to make sure it’s filed and pay by this new date? Or is it, or what do they need to worry about Steven?

Steven: [00:24:09] Well, they’re required, actually, I call that a buffet, I call that a tax benefit buffet, a COVID-19 tax benefit buffet coming in from a different acts. Coming from CARES act, coming from your Family First act. And maybe they tried to attempt to add more in under the Hero’s act, but it did not pass. So there are a lots of things, I think I summarized eleven of them. I cannot remember them all right now. But once there is, you know, basically the IRS extended everything. Whatever you do before, it’s all extended for six months. Plus, the majority of the returns or forms are extend to July the 31st. July 15th, sorry. So you have enough time and then you don’t have to pay. The payment obligation is also extended. So you don’t have to pay. And besides that they have many other important benefits available that is worth, worth doing some tax planning. Now I want to make sure people understand the difference between tax preparation and the tax planning. So the biggest problem, Karl, you and I talk almost every week on this and before COVID-19 I was, try to always educate that to folks. Tax preparation is really a cost. Something you have to do. It’s like you’ve got all your information for last year. You give it to your tax preparer, put it in the software and then send it to IS, right. It’s just to report information you have. Tax planning is really, you have to look at lots of legal intricate structure and locality or personal life insurance, retirement, look at text, no tax costs different than the CARES act, all those things, and then come up sporadically, typically it’s done before the end of the year. For example, under the Family First Act and the CARES, they have lots of stuff. For example, they have lots of benefit. You can use, you can take advantage. One simple articles, called section 139. Section 139 was drafted really for section nine, really for 911, what time, you know, lots of victims of 911. So they passed the law. Basically say if there are certain victims, their family or your employees that are impacted by that tragedy, you can pay your employees a certain amount to really support a family, right? But the sentence was drafted as a national disaster. So if you’re paying your employee, because of national disaster, you can, the employer can pay a certain amount to the employee and the employer can deduct those expenses. An employee does not have to include that in their income. So it’s tax free for the employees. It’s almost like double dipping, right. But it is really for the tax, for the national disaster relief. So now we have another national disaster, COVID-19, so you can do the same. You can do the same for your employee, for example, you know Karl, literally I think a you and I both now with the kids at home, we really cannot work. So we can literally, we can pay the employee. You can hire a nanny for your employee to take care of their kids so they can work, right? Or you can pay for the internet service, so maybe computer or camera, if they are required to do that to work from virtual, right? Or if you have to buy certain, something to keep them safe. As long as those are necessary expense to help them to go through this thing. Those could have be tax deductible for the, for the employers, I mean, deductible for the employer and the tax free for the employee. That’s why. And there’s quite a few other things. For example, you can always, you can get the retention credit, right? You know, if you’re keeping employees, you can get a retention credit and you can defer your payroll tax for two years. So you know, those 15.3% you’d have to pay now. And QIP, that’s very important, but if you did some qualified improvement, you are allowed to write them off immediately, right? And also like if you have net operating loss in previous years and you can, you can just, they are allowing you to carry it back and then you can convert those net operating loss into cash now. So you can receive a check now. So we went through a change a little bit, when we do the tax plan before the, pre COVID-19, we always try to focus on how to save people money. But now we are not looking, not just at saving people money, saving people tax, but also helping them to generate cash. Bring the cash to your pocket right now, so.

Karl: [00:29:22] That’s a key thing that you highlighted a couple of great, great suggestions, but I know a lot of people are impacted with employees that have to work from home. At the same time, a lot of the childcare services that were traditionally available weren’t available or aren’t available. And so these are costs that people have to account for because of COVID-19. And if I understand you correctly, there might be opportunities where you can in addressing some of those things, there might be some tax advantages or tax things you need to understand and know that can be applied to help you and your business.

Steven: [00:30:05] Yeah. Huge advantages, especially the people involved in if they do, if they have some new manufacturing boards, they have some real estate warehouse related. There is more benefit out of that.

Karl: [00:30:16] So, you know, as you think about it, we we’ve started off by talking about, COVID-19 and all the loans that help push money into the economy. I’d like to ask you to maybe take out your crystal ball a little bit. And you’ve got a perspective on, you know, the future of both from you do a lot of business with international businesses that do business in China, North America, all over the world. What are you seeing and hearing, you know, over the next year, that business owners should be considering. How not, not so much how long this is going to last, but just what should people start preparing for when it comes to cash? The financials of their business over the longer term?

Steven: [00:31:06] What they, I would say it’s hard to predict what are the future looks like, but I think the chances are, you know, maybe yeah we’re gonna reopen. You know, maybe some, maybe school is gonna reopen in September, but eventually the risk of a second wave of infection is very high. If you’re considering given lots of negative, if you see people on the, right now into the protests. Lots of, lots of crowds. I mean, not a lot of them wear the masks. I feel like almost like the second wave is becoming evitable. So those are, how does that impact the business? I think we needed to really consider what, we have to plan out what if the second wave is true, will come? And does the business have to shut down again. How do you plan, right? How much, you have to look at, you know what if your business just returns to only 90% or 50% or 20% and how much cash you have? What if they use up all the PPPs? What if there’s no more free money from the government, right? How much your burn rate you have? How much money you have in your bank and how much money you have before you use up all your critical or other loans? So that’s the thing I think, as a, the business to think about, I know you do, they have to really think about it. And right now we do, we have the client do some forecasting budgeting. They look at your cash, you know earn rate and do some prediction on how much revenue you can incur that, how much to recover the revenue loss during the lockdown. And in the future, how much they’re sort of factoring the possibility of second wave. Anyway, it’s really become the exercise of doing a, doing a forecasting budgeting and getting prepared.

Karl: [00:32:59] This is critical. We just experienced about 11 to 12 year expansion, economic expansion. So there’s a lot of business owners that came into the business over that period of time. And they didn’t have to focus on the financials, the cashflow of their business for the last 10 years, because they were growing consistently. It was predictable. When you enter into a period of uncertainty and we don’t know the probability of a second wave, or even other things that are impacting the economy happening over the next 24 months. But planning the financial scenarios, what cash you need, what lending or borrowing or equity injections is going to be needed, where you need to pivot your business. How much will that cost to do. If you need to remodel your restaurants to enable social distancing from its current floor plan, you might need a general contractor and other funding that. There are mechanisms to fund that, but you need a plan, financial plan for your business to be able to do that. And that’s where if you have the skill set and knowledge to manage the financial of your business, now’s the time to use it. If you don’t have that knowledge and skill, now’s the time to learn it or to reach out to people that can help you. Your business might depend on it over the next 24 months. So I think it’s wise advice that you describe the role of a CFO in your business, no matter their size. Because it’s looking forward on how to plan for the financial needs of your business versus rearward looking on what did you do last year and how much taxes you owe. So really appreciate you sharing some of those ideas and tips with us. How would people get in touch with you if they wanted to learn more about tax planning, COVID-19 financial planning and others.

Steven: [00:35:02] Well, if they’re already connect with you, you know, just send you an email, but I can also be reached by steven@gucpagroup.com. That’s my email. And I do either a one point, Karl and Rico, you probably agree with me on this. I call myself a war time, COVID-19 war time CFO. Really we have to plan ahead, but I think we will never return to what we were three months ago, or even maybe six months ago. We will never. Because look at, we have 38 million in unemployment. Think about that. Even if we add 1 million a month at an average of one million a month, that’s going to take 38 months. Probably we will never again, we will never return to what we used to be. So we really need to plan. We need to plan ahead.

Rico: [00:35:56] I agree with you that we need to plan ahead. I’m hoping that we do return at some point somewhere. It might take a year. It was that boom economy for the last 10 years, like Karl said, can be a bit tough to do that anytime soon, I’m sure.

Karl: [00:36:14] Or industries will change. I think, you know, we are able to adapt. That is one thing that both here in America and around the world, we adapt to changes. After 911 flying on planes were different, but they, the people flew again and people travel and new industries emerge. Uber is a post 911 industry that, that flourished and there’ll be others. For the business owners that are out there trying to navigate today. The goal is survival. But also start looking forward to how to change the nature of your business for what the future may look like. Those that are able to do that faster, they’re going to be more successful in the long run.

Rico: [00:37:02] Especially with businesses like Steven said that have to look at maybe a second wave coming. So just be prepared. If you’re going to have to close down again, if that’s what we have to do,

Steven: [00:37:13] Right. Again, not all the business were impacted all the same. Some are really, they probably could have, cannot survive. Some are just impacted a bit, they can bounce back. But some are, is just a beneficiary out of the COVID-19, the Ecommerce, you know, some health care. You, know, it’s different.

Karl: [00:37:31] Well, again, I’d like to thank Steven Gu. He is the founder and CEO of a Gu and Company, a fractional CFO tax and business advisory firm. You shared a lot of great information. For some people you know, this might highlight some opportunities where they can get more precise and efficient with how they run their business and whether they reach out to their accountant or anybody else, or reach out to you. It’s time for folks to really pay attention to this important aspect. If nothing else taught us a lesson, when the government had free money to give out those that knew what to do and how to do it, and those that had their books and records and good accurate business records, they got to the front of the line, they got the money quicker. And so should that happen again, people have a personal mission to look at their own situation and see if they can make some improvements. So they’re more ready for the next, the next time. Thank you very much. We’d like to thank everybody for tuning in to the Capitalist Sage podcast we’re continuing to have new and interesting guests come in and talk about things to help you improve your business. I’m Karl Barham with Transworld Business Advisors, Atlanta Peachtree. And believe it or not, this has been a time where people have reevaluated what’s important in life and we have more qualified buyers and investors in businesses that you would think. People are looking to invest in different businesses. And we help them find the right business. If you’re a business owner and you decided that, you know, you want to move on to other things in your life. There is a process to help get your business sold so that you can do what’s next. And so feel free to contact myself, one of my agents. We’ll be able to help you with that. You can reach us at KBarham@TWorld.com or visit our website www.TWorld.com/AtlantaPeachtree. Rico, why don’t you tell us a little bit about what you’ve got coming up?

Rico: [00:39:41] Sure. Before I get to that. Steven don’t don’t log off when we sign off, hang in there for a few minutes. And for those that need Steven Gu’s information, I’ll make sure it’s in the show notes also. So you can track back to his Facebook or LinkedIn pages, or certainly reach out to me or call. But you know, Peachtree Corners magazine. The newest issue is in the mailboxes. I got mine today, so hopefully everyone’s getting them their copy over the next few weeks. We’ve been fortunate to have a support of the city, local businesses continuing to advertise. So it’s a strong issue. This one’s about, stories that brighten our spirits. So a lot, a lot of people doing a lot of different things during COVID-19. People making, so Steven Shininess is our cover story, along with four other stories of people that have decided to do different things than what they were originally doing. So he’s 3D printing face masks. Howill Upchurch is a videographer, but he also creates guitars. So he was making guitars in his workshops. And there’s a bunch of people like that. Lots of stories. So pick it up. You could pick it up at, there’s still places that are carrying the publication that are able to do it in this COVID-19 environment. So check them out. Dunkin Donuts, Ingles, lots of restaurants that are opened for dining. You’ll see, you’ll see it there. Or go to living in PeachtreeCorners.com, you can find the digital edition there. Mighty Rockets, that’s what I do, social media, videography and all that. We’re still doing gangbusters, so there’s a lot of work out there for what I’m doing for companies. I need to get online, whether they’re doing a webinar or podcasts or other things, I’m busy doing that. So MightyRockets.com. You can email me Rico@mightyrockets.com and I’ll help you guys out.

Karl: [00:41:40] Well, thank you again, Steven for joining us today. And for everybody out there, stay strong. Keep pushing forward. Take care. Have a great day.

Scottt Gottuso and Geoffrey Wilson. Photo provided.

Peachtree Corners will soon lose one of its most iconic, popular and tasty businesses.

Peterbrooke Chocolatier, run by Geoffrey Wilson and Scott Gottuso, has been told by Peachtree Forum landlords, North American Properties and Nuveen Real Estate, that its lease will not be renewed. The last day of business will be July 25.

Meanwhile, Peachtree Forum is getting several new stores. They include Kendra Scott, Sucre, and The NOW Massage. Previously announced were Alloy Personal Training, Cookie Fix, Gallery Anderson Smith, Giulia, Lovesac, Nando’s Peri-Peri and Stretchlab. Wilson adds: “We are not in their big picture.”

Wilson has operated Peterbrooke at the Peachtree Forum for 14 years and Gottuso has been there nine years. They have made the chocolatier profitable and doubled sales. Wilson says: “We turned it around through community involvement and made relationships. We worked with the schools, gave donations, did a lot in the community, and made a difference. We produce most everything we sell in the shop, so it’s labor intensive. We make European-style chocolate treats from scratch from the very best ingredients, package it, make gift baskets, and also sell a lot of gelato.”

Key items include truffles, hand-made caramels, cherry cordials, chocolate-covered cookies and pretzels and strawberries hand-dipped in their own blend of chocolates. (They are all good!) One of Wilson’s and Gottuso’s most iconic products is chocolate popcorn. Once you try it, regular popcorn is tasteless. “We sell a lot of it.” Wilson adds: “Gelato sales have carried us in the summertime, since there are not many chocolate holidays in the summer.”

Peterbrooke now has five employees, and would like to have 10, but it is difficult to hire people with the skills in chocolatiering. A key part of its business is corporate companies, such as Delta Air Lines and Capital Insight. The Peachtree Corners’ Peterbrooke has corporate customers as far away as Cleveland, Ohio.

The operators were surprised when the Forum owners did not renew its five year lease. “The big decisions were made in Charlotte or Cincinnati, not locally,” Wilson feels. “We were no longer in their big picture. They want new and glitzy, shiny, fancy and trendy.”

The operators plan to start their own chocolate company, to be called “Scoffrey,” and initially sell online, plus have pop-up locations during holidays, and possibly have a booth in other merchants’ stores on occasions.

“Whatever we do would look different. We might rent a space somewhere close by so that people can still have the good chocolate experience with us, but we won’t have a regular audience walking by.”

Another element: the price of chocolate futures has spiked this year, with a bad crop production year. Wilson says: “That is key to our business and a huge cost increase. That doesn’t help.”

Wilson adds that the forced closing of the Peterbrooke location “is something like the death of a friend. But you go to the funeral and to the wake, and in six months or a year, It won’t be so bad.”

This material is presented with permission from Elliott Brack’s GwinnettForum, an online site published Tuesdays and Fridays. To become better informed about Gwinnett, subscribe (at no cost) at GwinnettForum

The Andrews Brothers performing at Avenue East Cobb via Instagram @avenueeastcobb

North American Properties (NAP) has revamped the Avenue East Cobb shopping center in Marietta, boosting its appeal to suburban residents seeking a more urban lifestyle. Now, it’s being honored as part of the Atlanta Business Chronicle‘s “Best in Atlanta Real Estate” coverage.

NAP is known for transforming properties like Atlantic Station, Colony Square and The Forum.

According to the Atlanta Business Chronicle, the redevelopment involved demolishing part of the main building to build a public plaza with a stage surrounded by restaurant patios.

A new concierge facility was also added, including a canopy for drop-offs. Additionally, smaller retail buildings were created for standalone tenants. The business mix was updated to include names like Warby Parker, Lululemon and Peach State Pizza.

NAP also increased community engagement by partnering with at least 10 local organizations for social events. These efforts have proven successful. Over the last two years, Avenue East Cobb has seen a 36% increase in sales per square foot thanks to a major rise in foot traffic.

More news from North American Properties can be found here.

North American Properties (NAP) and Nuveen Real Estate announced three new businesses coming to The Forum Peachtree Corners (The Forum). The new brands include Kendra Scott, Sucré, and The NOW Massage.

“We’re excited to keep expanding our merchandising mix with more experiential concepts that motivate guests to extend their time on property. In addition to these new leases, several tenants are on track to open over the next few months, and we can’t wait to see the impact,” said Brooke Massey, director of leasing at NAP.

Here are the latest deals to be signed at The Forum:

Kendra Scott – Known for its plethora of accessories and customizable Color Bar experience, jewelry brand Kendra Scott blends classic designs with modern sophistication. Kendra Scott jewelry celebrates individuality and self-expression.

The growing brand has also donated over $50 million to local, national and international causes since its launch in 2010. The 2,284-square-foot space, situated next to Lovesac, opens later this spring, marking the retailer’s fourth location in the NAP portfolio.

Sucré – Founded in New Orleans, Sucré is a gourmet patisserie known for its macarons, gelato and other handmade, French-inspired desserts.

The sweet boutique will occupy a 1,718-square-foot space on the north end of the property and is slated to open later this year. Georgia is the brand’s first out-of-state venture, with The Forum being its third metro Atlanta location and eighth overall.

The NOW Massage – This brand is helping people discover the healing benefits of massage therapy.

The customizable menu offers guests three signature massage styles and a variety of exclusive enhancements like Deep Tissue, Herbal Heat Therapy, Hemp Calm Balm, Gua Sha, Gliding Cupping and more. Located near Mojito’s, the 2,414-square-foot massage boutique debuts late summer.

These businesses join:

Alloy Personal Training (opening this month), Cookie Fix (open), Gallery Anderson Smith (opening this month), Giulia (opening this spring), Lovesac (open), Nando’s Peri-Peri (coming winter 2024), and Stretchlab (open).

Since acquiring the property in March 2022, NAP has executed 39 deals with new, existing and temporary tenants alike.

Parks & Recreation1 week ago

Parks & Recreation1 week ago